Buying a home is one of life’s biggest decisions—and doing it as a couple adds layers of opportunity and complexity. Here’s how to weigh your options:

1. Financial Flexibility & Affordability

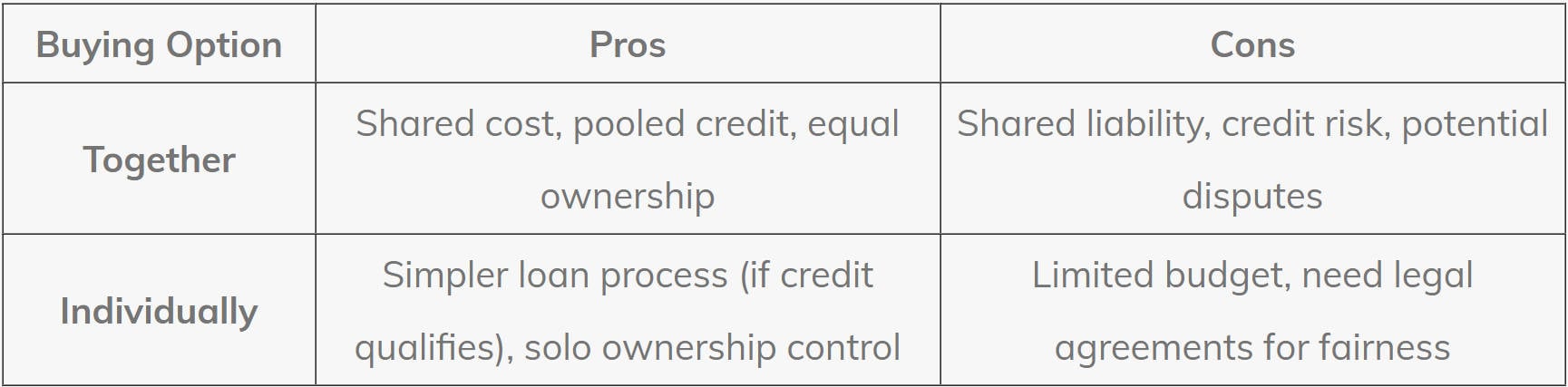

Buying together often means combining incomes and credit strengths to secure a larger mortgage or better rates. You can also split closing costs and monthly payments.

Buying individually allows one partner to qualify alone, which can make sense if the other has credit issues, high debts, or limited savings. But going solo might restrict your budget or mortgage flexibility.

2. Credit History & Mortgage Application

Joint application means both credit histories impact approval. If one partner has weaker credit, you could be taxed with higher interest rates—unless you opt for a co-borrower arrangement.

Separately, the higher-scoring partner applies on their own, potentially unlocking better loan terms. Yet this also limits who legally shares ownership, unless protected via other agreements.

3. Ownership Rights & Legal Considerations

When you buy jointly, property ownership typically becomes tenants-in-common or joint tenants, ensuring both parties legally own the home—helpful for estate planning and shared equity.

If one person buys individually, drawing clear agreements on financial contributions, ownership rights, and exit strategies becomes vital. These can include cohabitation agreements, title arrangements, or future buy-outs.

4. Relationship Dynamics & Exit Plans

Relationships evolve, so think ahead:

- Who covers mortgage if one partner can’t?

- What if one wants to sell or move on?

- Agreements like “right of first refusal” can avoid conflict later.

Buying individually gives one more financial control, but lacks shared protection unless legal safeguards are set in place.

5. Market Conditions & Timing

The U.S. housing market has recently shifted toward a more buyer-friendly environment, with cooling prices and more seller concessions compared to early 2025 Business Insider +1. Mortgage rates have dipped slightly, boosting affordability and creating new opportunities for eligible buyers Realtor.

These conditions might favor solo buyers looking to act quickly, but joint buyers may find the market timing even more compelling.

Summary Table

Final Thoughts

Couples should evaluate credit profiles, legal ownership, long-term relationship direction, and financial goals. If both partners bring strong credit and stable incomes, buying together can maximize buying power and build shared equity.

But if one partner’s financial situation complicates the mortgage or you value independent ownership, buying individually—with legal safeguards—is a smart path. No matter which route you choose, communicating clearly and possibly consulting a real estate attorney or financial advisor ensures peace of mind—and smoother ownership ahead.

Compliments of Virtual Results